MaxDecisions: US consumer credit FICO score drops as delinquency rises in 2023

Credit Score

MaxDecisions: US consumer credit FICO score drops as delinquency rises in 2023

Research overview

We tracked nearly 170 million US consumer over a period of 16 months from June 2021 to Oct 2022. MaxDecisions research staff have found that deep subprime, subprime or near prime US consumers have experienced a significant deterioration in their credit score due to inflation and unemployment.

Economic overview

US consumer spending hasn’t stopped despite a number action taken by the US Federal Reserves. During the global pandemic from 2019 to 2022, there were major disruptions to the global supply chain causing unpredictable rises in cost across the board.

From consumer goods, energy to large ticket items such as consumer appliances and cars, we see a rise in cost across the board. The US Federal Reserves and other nation’s central banks have been consistently raising borrowing rates to cool down spending or demand of these consumer goods to lower prices.

Raising interest rates or borrowing rates doesn’t fix some of the aforementioned supply chain issues but it does create difficulties for consumers to borrow money and therefore artificially decrease demand for these consumer goods.

Inflation and corrections

Inflation has slowed due to these monetary policies but the increase in prices are still felt throughout the economy, especially basic consumer goods such as eggs. Consumers across the world still needs to spend money to maintain their life styles and the places to turn to to sustain that life style are credit cards.

Credit card companies have raised from an average of 16% to 19% in less than 12 months. Although this is expected, the consumer still needs to buy eggs for breakfast and some of the consumers on the lower end of the income and credit spectrum are getting the short end of the stick.

With the looming lay offs of 2022 and 2023 in the tech sector, the cascading effects are felt even more strongly in the subprime sector.

Numbers and Analysis

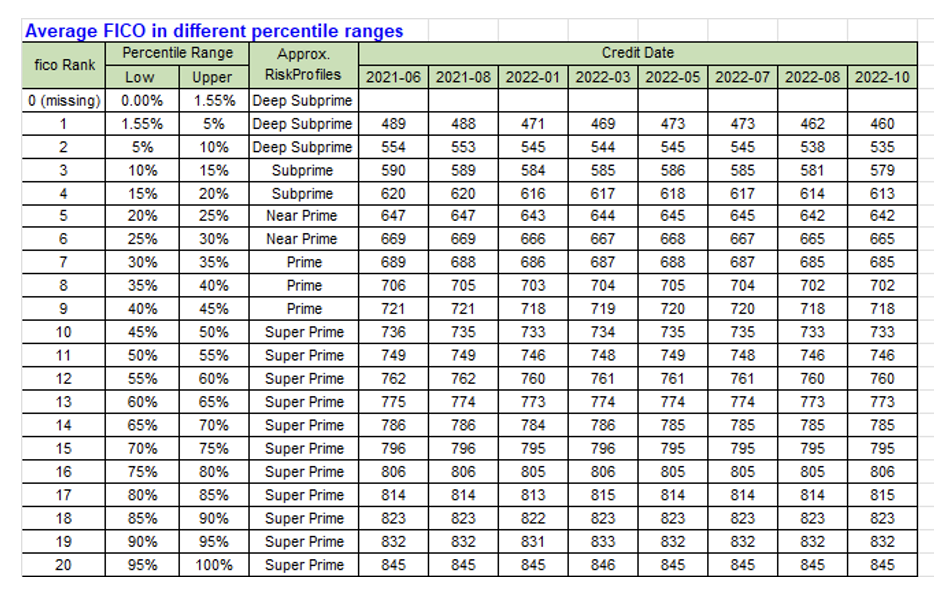

We sampled over 180 million US consumers over a year and a half from June 2021 to Oct 2022. And from a border perspective, average FICO score fell give points on average from 720 to 715. This drop in FICO score is a reflection at the inflection point in June 2021 when inflation rises to an uncomfortable 7 to 9% month over month metric.

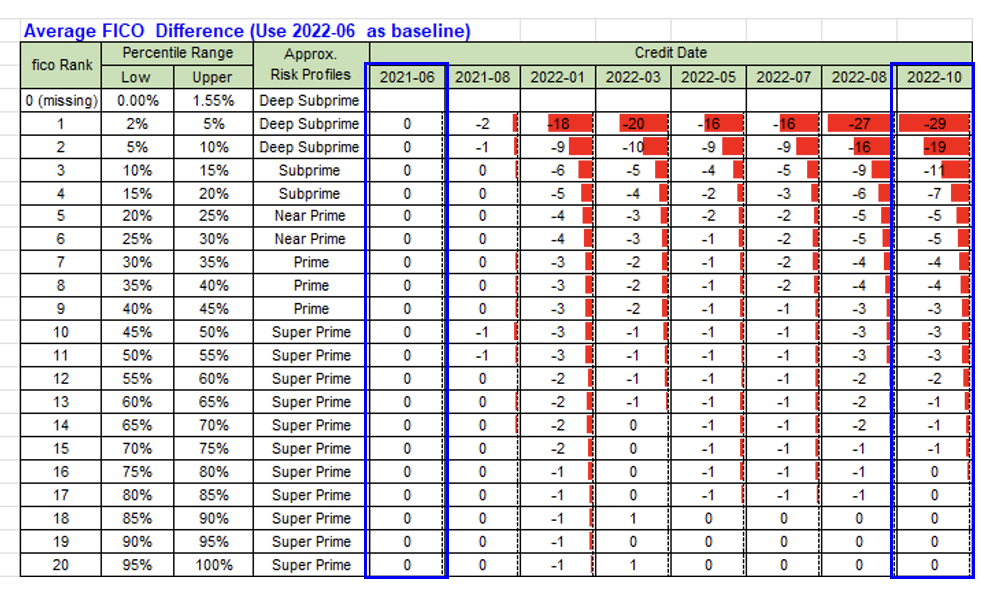

More over, if we stratify FICO scores from best (20) to worse (1), we see a more dramatic drop in the lower credit bands. In other words, the subprime sector of the US population are experience as much as 20 point drops using June 2021 as a baseline.

You can see that FICO ranking bands of 1,2,3,4,5 from FICO 480 to FICO 650, there is a corresponding drop of FICO score from 5 to 20.

Corrective action

Lenders should think about adjusting underwriting rules and criteria to maintain a certain credit quality for their applicants. Expect a higher than expected cost per customer with a higher marketing spend. Lenders conversion rate will be impacted as such and we expect this trend to last at least until the end 2023.

For those service organizations in the debt consolidation and debt management space, expect a higher number of contacts from consumers looking for credit counseling and debt management.

Next time, we will share some of the delinquency percentages and give everyone a perspective on the severity of US consumer credit defaults that are happening as we speak.

MaxDecisions Research Team

Credit Score

Direct mail marketing has been around for ages. The original free way to get your products and services in front of your audience without having to pay Google, Facebook and other online services an exorbitant amount of money with limited to no control on how their algorithm really works.